The $30 Trillion AI Reckoning: Why Software Stocks Just Had Their Worst Week Since 2008, Claude Cowork Sparked the “SaaSapocalypse,” and What It Means for Your Job

Eight Days of Losses. $285 Billion Wiped Out in One Session. And a Warning That Financial Institutions Could Lose $30 Trillion if the AI Bubble Bursts. Here’s What’s Really Happening—And How to Prepare.

Published: February 9, 2026 | Last Updated: 1:32 PM AEST | Reading Time: 18 minutes

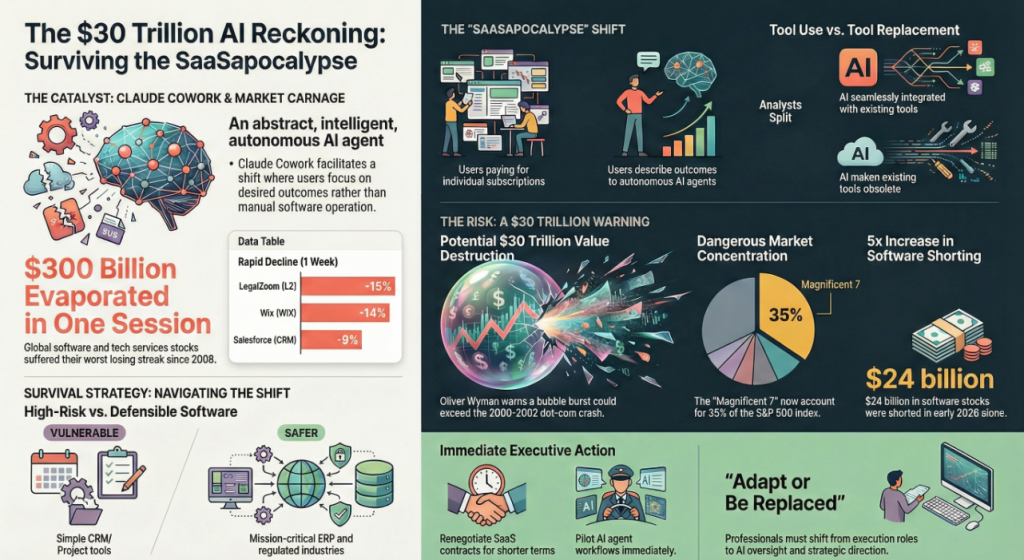

The S&P 500 Software & Services Index just closed its eighth consecutive day of losses—the worst losing streak in nearly six years—with the sector down 19% over that period alone.

In a single session last week, $285-300 billion in market value evaporated from global software and tech services stocks after Anthropic announced Claude Cowork, an AI agent that can handle complex professional workflows that many software companies currently sell as their core products.

Thomson Reuters, Salesforce, LegalZoom, Workday, monday.com, Wix—all hammered. Asian IT giants Tata Consultancy Services and Infosys caught in the downdraft. Even chip designer Arm Holdings wasn’t spared.

And now, management consulting firm Oliver Wyman has issued a stark warning: Financial institutions face the risk of losing more than $30 trillion in market value if the AI bubble—which has driven valuations to unprecedented levels—suddenly bursts.

This isn’t just another market correction. It’s a fundamental reassessment of which companies can survive in an AI-first world—and which business models are about to become obsolete.

But here’s where it gets interesting: Nvidia CEO Jensen Huang calls the panic “the most illogical thing in the world.” Industry analysts are split between those predicting a “SaaS apocalypse” and those arguing this is overblown fear.

So what’s really happening? Is this the end of software as we know it? Or is it a massive overreaction that presents the buying opportunity of the decade?

What Triggered the Panic: Claude Cowork and the End of “Software as a Service”

The Anthropic Announcement That Started It All

On January 30, 2026, Anthropic unveiled Claude Cowork—and within hours, software stocks began cratering.

What is Claude Cowork?

Claude Cowork is an AI agent (not just a chatbot) that can:

- Analyze complex data across multiple sources

- Draft legal documents with context from hundreds of precedents

- Prepare meetings by pulling information from emails, calendars, documents

- Handle administrative tasks end-to-end without human intervention

- Reorganize file systems, clean inboxes, generate reports

- Build presentations from scratch using data, research, and company templates

- Run multi-step workflows across tools (Google Drive → Docs → Sheets → Web → Back)

- Browse the web and pull fresh, current information

- Ask clarifying questions when instructions are ambiguous

Here’s the key difference: You don’t open apps. You describe outcomes.

Instead of logging into Salesforce to update a CRM record, then switching to Google Sheets to pull data, then opening Slack to notify your team—you tell Claude: “Update the quarterly sales pipeline with last week’s closed deals and notify the team.”

And it does it. All of it. Autonomously.

Why This Is Different from Previous “AI Hype”

“This is literally what Microsoft Copilot and ChatGPT Desktop should have been,” wrote LinkedIn AI analyst Linas Beliunas. “This isn’t a feature. It’s a replacement.”

The scary part for software companies:

Claude Cowork was 100% built by Claude itself. Anthropic shipped it in approximately 1.5 weeks using Claude Code. AI is now building AI tools to make AI even more useful—and it’s doing it faster than human engineers ever could.

Early testers report:

- 80%+ time savings on contract review

- Automated RFP responses that previously took days

- Tier 1 customer support handled entirely by agents

As one analyst put it: “Whoever owns the agent layer wins 10x the budget.”

The “SaaSapocalypse” Is Born

Within 48 hours of the announcement, a new term emerged on financial Twitter: SaaSapocalypse = “SaaS” + “apocalypse.”

The fear: Anthropic’s AI agents could obliterate the $500 billion+ SaaS + IT services market by automating entire workflows—not just individual tasks.

Reddit user on r/Anthropic: “CoWork plugins wipe billions off global market in ‘SaaSapocalypse.’ Huge selloffs in software globally and people are attributing this to Claude.”

Calcalistech reporting on Israeli tech stocks: “Anthropic’s Claude Cowork triggers fresh doubts over subscription software, wiping billions from Wix and monday.com.”

Fast Company headline: “Why one Anthropic update wiped billions off software stocks.”

The market’s brutal logic:

If one AI agent can replace:

- CRM software (Salesforce, HubSpot)

- Project management tools (Asana, monday.com, Jira)

- Legal research platforms (Thomson Reuters, LexisNexis)

- Analytics tools (Tableau, Looker)

- Customer support software (Zendesk, Intercom)

- HR systems (Workday, ADP)

…then why would companies continue paying $500-$2,000 per seat per year for each tool?

The implication is unsettling for a sector built on the idea that every business process requires a dedicated software platform.

The Numbers: Just How Bad Is It?

Software Stock Carnage (February 2026)

S&P 500 Software & Services Index:

- 8 consecutive days of losses (longest losing streak in 6 years)

- Down 19% over 8 days

- Down ~20% year-to-date (as of Feb 5)

- 102 of 114 constituent stocks fell in Thursday’s session alone

Single-session wipeout (Feb 4-5):

- $285-300 billion in market cap evaporated globally in one session

Individual stock performance (week of Jan 30 – Feb 6):

| Company | Ticker | Approximate Decline | Business Type |

|---|---|---|---|

| Thomson Reuters | TRI | -12% | Legal/financial research |

| Salesforce | CRM | -9% | CRM software |

| LegalZoom | LZ | -15% | Legal services platform |

| Workday | WDAY | -11% | HR/finance software |

| monday.com | MNDY | -13% | Project management |

| Wix | WIX | -14% | Website builder |

| Tata Consultancy | TCS | -8% | IT services |

| Infosys | INFY | -7% | IT services |

Hedge fund activity:

- $24 billion in software stocks shorted in 2026 alone (as of Feb 4)

- 5x increase from previous two years combined

The “Magnificent 7” Concentration Risk

Oliver Wyman’s analysis highlights a deeper structural problem: unprecedented market concentration around AI-related companies.

The Magnificent 7:

- Apple, Microsoft, Amazon, Alphabet (Google), Meta, Nvidia, Tesla

- Collective valuations increased nearly 8x since January 2020

- Now account for 35% of the S&P 500

- Concentration comparable to peak of dot-com bubble

Current U.S. equity market cap:

- Nearly 2x the size of GDP

- Far higher than at the peak of the dot-com era

- Suggests potential fallout could exceed 2000-2002 crash

AI infrastructure investment acceleration:

- $6+ trillion in funding required between now and 2030 (JP Morgan estimate)

- Covers: AI data centers, energy projects, supply chains

- AI-driven infrastructure investment accounted for 92% of U.S. GDP growth in H1 2025 (Harvard economist Jason Furman)

Forbes summarizes the current market as “a $2.52 trillion AI bubble” with spending forecast by Gartner to reach $2.52 trillion in 2026—a 44% year-over-year increase.

The $30 Trillion Warning: How Bad Could It Get?

Oliver Wyman’s Nightmare Scenarios

Management consulting firm Oliver Wyman published a research note warning that financial institutions “can’t afford to ignore the growing risk of an artificial intelligence bubble that could ultimately destroy more than US$30 trillion in market value.”

Two potential collapse scenarios:

Scenario 1: Equity Market Correction (The “Soft” Crash)

Trigger: Sudden shift in investor sentiment around AI’s ROI potential

Mechanism:

- Investors realize AI returns aren’t matching investment levels

- Sharp equity market correction across tech sector

- Falling business investment as companies cut AI budgets

- Declining household wealth (retirement accounts, 401ks)

- Rising unemployment as tech layoffs cascade

- Significant recession

Historical comparison:

- 2000-2002 dot-com crash: NASDAQ fell 80%, S&P 500 dropped 50%

- $6 trillion in equity value wiped out (in 2000 dollars)

- At current market levels, comparable crash would destroy ~$33 trillion—more than the entire U.S. economy

Oliver Wyman: “If this scenario sounds familiar, that’s because we lived through an equity scenario in the aftermath of the dot-com bubble.”

Scenario 2: Debt-Fueled Collapse (The “Nuclear” Option)

Trigger: Widespread defaults across complex credit markets

Mechanism:

- AI investment increasingly financed through borrowing (not cash reserves)

- Downturn triggers defaults by hyperscale tech companies

- Private credit markets collapse ($1+ trillion AI-related debt at risk)

- Banks discover far more exposure than internal reports suggested

- Credit contagion spreads beyond tech sector

- Financial crisis comparable to 2008

Warning signs already visible:

- Bond issuance by hyperscale tech companies exceeded $100 billion in past 6 months

- More than 5x the level of previous two years combined

- Private credit markets heavily involved: $1+ trillion of AI-related debt expected through alternative lenders

- Hidden concentrations: Banks may own far more data-center and digital infrastructure risk than they realize

Oliver Wyman: “In 2008, banks discovered they owned far more US housing risk than their internal reports suggested. They might soon discover the same about data-center and digital infrastructure risk.”

“The more leverage, the more fuel, the hotter the fire,” the report warns.

The “More Moderate” Outcome Still Involves Pain

Oliver Wyman acknowledges a moderate scenario where:

- Some SaaS companies survive by pivoting to AI-orchestrated workflows

- Software margins compress but don’t collapse

- Gradual transition rather than catastrophic crash

But they warn that geopolitical instability, supply-chain disruptions, and rising public debt could amplify any downturn.

“There is little room for complacency,” the firm concluded. “Firms that act early to execute hedges and diversify portfolios will be best positioned to weather the storm.”

The Great Debate: Is This Panic Justified or “Illogical”?

Team “This Is Overblown”: Nvidia CEO Jensen Huang

At an event on February 3, Nvidia CEO Jensen Huang called the software sector panic “the most illogical thing in the world.”

His core argument:

“There’s this notion that the software industry is in decline and will be replaced by AI. Remember what software is? Software is a tool. It is the most illogical thing in the world, and time will prove itself.”

Huang’s “ultimate thought experiment”:

“Suppose we achieve artificial general robotics, the ultimate AI, the physical version of us. You could, of course, solve any problem because you’re humanoid. You could do things if you were a human robot.

But would you reinvent a hammer? Would you reinvent a screwdriver? Would you reinvent a chainsaw? Of course not. You would use the tools.

And so now do the digital version of that. If you were an artificial general intelligence, would you use the tools like ServiceNow and SAP and Cadence and Synopsys, or would you reinvent a calculator? Of course, you would just use a calculator.

That’s the reason why the latest breakthroughs in AI is what? Tool use, because the tools are designed to be explicit.”

Huang’s thesis:

AI systems, even at their most advanced, will require the structured, reliable tools that software companies provide. Rather than replacing software, AI will become a more sophisticated user of it.

Rene Haas, CEO of Arm Holdings, echoed this sentiment, describing recent market fears as “micro-hysteria” and arguing that enterprise AI deployment is “still in its early days and not yet massively transformative.”

Wedbush Securities agrees:

In a February 5 research note, Wedbush called the selloff an “Armageddon scenario for the sector that is far from reality.”

“Enterprises won’t completely overhaul tens of billions of dollars of prior software infrastructure investments to migrate over to Anthropic, OpenAI, and others. Large enterprises took decades to accumulate trillions of data points now ingrained in their software infrastructure.”

Team “This Is the Beginning of the End”: The SaaS Bears

Opposite view from multiple analysts:

Melius Research: “AI is going to eat software.”

Constellation Research: “The sell-off reflects concerns that AI could pressure profits and limit how much software companies can charge.”

Futurum Group’s Rolf Bulk: “There’s likely to be cannibalization of SaaS by AI-driven workflows and that will impact the multiple the sector trades on.”

The bear case logic:

- Agents replace workflows, not just tasks: Previous AI tools automated individual steps. Claude Cowork orchestrates entire processes end-to-end.

- Margins will compress: Even if SaaS companies survive, they’ll face massive pricing pressure. Why pay $2,000/seat/year when an AI agent can do the same work for $200?

- “Per-seat” pricing model is dead: Software has been priced by number of users. But if one AI agent does the work of 10 employees, revenue collapses by 90%.

- Switching costs are lower than bulls think: Yes, enterprises have invested billions in infrastructure. But if AI agents can integrate with existing systems via APIs, companies can gradually replace tools without massive overhauls.

- The “tool use” argument is backwards: Huang says AI will use existing tools. Bears say AI will build its own tools optimized for AI workflows, not human interfaces.

Reddit developer perspective:

“Claude Cowork doesn’t need Salesforce’s UI. It needs Salesforce’s data. Once Salesforce realizes this and pivots to ‘database + API access’ at 1/10th the price, their revenue model collapses.”

The Middle Ground: Some Software Survives, Some Dies

Rolf Bulk (Futurum Group) offers nuance:

“A subset of software providers, especially those running mission-critical enterprise workloads such as Oracle and ServiceNow, still have a sustained ‘right to earn.’ The depth of their data and entrenched role in customer workflows make them more likely to coexist with AI rather than be replaced outright.”

The survival checklist:

✅ Mission-critical workloads (can’t be easily replaced without business disruption)

✅ Deep, proprietary data (decades of customer-specific information)

✅ Regulated industries (compliance requirements create switching barriers)

✅ Network effects (value increases with more users)

✅ AI-native pivot (companies that rebuild products around AI agents)

AlphaSense SVP Chris Ackerson:

“The future belongs to providers that combine advanced AI with trusted content, explainability and deep domain context.”

What This Means for Different Stakeholders

For Software Company Employees: Should You Be Worried?

Short answer: It depends on your company and role.

High-risk companies:

- Single-feature SaaS tools that can be easily replicated by AI agents

- Project management software (Asana, Trello, monday.com) — agents can coordinate tasks

- Basic CRM platforms without deep customization or integrations

- Simple analytics dashboards — AI can generate these on-demand

- Tier 1 customer support platforms — agents handle this better already

- Meeting scheduling/coordination tools (Calendly, etc.) — trivial for agents

Lower-risk companies:

- Enterprise resource planning (SAP, Oracle) with decades of customer data

- Regulated industry software (healthcare, finance) with compliance requirements

- Developer tools and infrastructure (GitHub, AWS, Snowflake) — AI uses these

- Deep vertical SaaS with proprietary workflows specific to industries

- Security and compliance platforms — still require human oversight

What employees should do NOW:

- Assess your company’s “AI defensibility”: Can your product be easily replaced by an AI agent? Or does it have deep moats?

- Develop AI-native skills: Learn to build, manage, and orchestrate AI agents rather than competing with them

- Pivot your role: Shift from execution to oversight, quality control, and strategic direction

- Update your resume and network: Even if your company survives, layoffs are likely as productivity per employee increases

- Diversify your assets: If you’re heavily invested in your company’s stock options, consider reducing exposure

- Consider career pivots: AI-resistant roles include complex problem-solving, creative work, human relationship management, and strategic planning

For Investors: Is This a Buying Opportunity or Time to Sell?

The bull case for buying the dip:

✅ Historical precedent: Every major tech panic in the past 20 years (dot-com crash, 2008 financial crisis, COVID crash) was ultimately a buying opportunity

✅ AI will expand the market: Even if individual companies struggle, total productivity gains from AI will create more wealth overall

✅ Jensen Huang is usually right: Nvidia’s CEO has been remarkably prescient about tech trends

✅ Valuations now more reasonable: 20% sector decline brings multiples closer to historical averages

✅ Survival bias: Companies that adapt will emerge stronger with less competition

The bear case for staying away:

❌ This time really is different: Agent-based AI is fundamentally more disruptive than previous technologies

❌ More downside ahead: 20% decline could easily become 50-80% if revenue models collapse

❌ Debt levels unprecedented: Leverage amplifies downside risk if AI ROI doesn’t materialize

❌ Market concentration extreme: When the Magnificent 7 inevitably correct, collateral damage will be severe

❌ No floor in sight: Traditional valuation metrics (P/E ratios, revenue multiples) don’t apply when business models are being replaced

What smart investors are doing:

- Shorting pure-play SaaS with weak moats (note: $24B already shorted, so crowded trade)

- Going long on “AI-native” pivots (companies rebuilding products around agents)

- Overweighting AI infrastructure (chips, cloud, data centers) vs. AI applications

- Hedging with options rather than outright selling

- Diversifying into defensive sectors (utilities, healthcare, consumer staples)

- Waiting for capitulation before deploying capital

Oliver Wyman’s advice:

“Conduct rigorous scenario analysis, identify hidden concentrations, and assess the impact of a potential 30 to 50 per cent equity market fall. Firms that act early to execute hedges and diversify portfolios will be best positioned to weather the storm.”

For Business Executives: Strategic Decisions in the Next 90 Days

The dilemma:

- Option A: Bet on AI agents replacing your software stack → Risk wasting money if agents don’t deliver

- Option B: Ignore AI agents and renew SaaS contracts → Risk being disrupted by competitors who moved faster

What forward-thinking executives are doing:

1. Run parallel experiments (Q1 2026):

- Keep existing SaaS tools running

- Pilot Claude Cowork, GPT-5.3-Codex, or similar agents on non-critical workflows

- Measure actual productivity gains vs. marketing claims

- Document what works and what fails

2. Renegotiate SaaS contracts (Now):

- Shorter contract terms (annual instead of 3-year)

- Per-usage pricing instead of per-seat where possible

- Include AI integration clauses allowing early termination if agents replace functionality

- Demand steep discounts citing market conditions

3. Invest in AI literacy for leadership (Q1-Q2 2026):

- Ensure C-suite understands capabilities and limitations of current AI agents

- Bring in independent advisors (not just vendors selling solutions)

- Run internal workshops on prompt engineering and agent orchestration

- Develop internal “AI strategy” function

4. Prepare workforce for transition (Ongoing):

- Transparent communication about AI adoption plans

- Reskilling programs focused on AI oversight and quality control

- Gradual workflow transitions rather than abrupt replacements

- Create “AI augmentation” roles where humans + agents collaborate

5. Reassess build-vs-buy economics (Q2 2026):

- Custom software now 10-100x cheaper with AI agents building code

- Projects previously outsourced may now be economical in-house

- But watch for “technical debt at AI speed” — systems built quickly without oversight

The Historical Parallel: Lessons from the Dot-Com Bubble

What 2000-2002 Teaches Us About AI in 2026

Similarities:

✅ Euphoric valuations disconnected from fundamentals: Dot-com companies trading at 100x revenue; AI companies today at similar multiples

✅ “This time is different” narrative: In 2000, “internet changes everything”; in 2026, “AI changes everything”

✅ Massive infrastructure investment: Fiber optic cables in 2000; data centers and chips in 2026

✅ Market concentration: Cisco, Oracle, Microsoft dominated; today it’s Nvidia, Microsoft, Google

✅ Extreme predictions: Gartner predicted $7.29T B2B eCommerce by 2004 (actual: $2-3T); today predicting $2.52T AI spending in 2026

Differences:

❌ Profitability: Many dot-com companies had zero revenue; today’s AI companies are profitable

❌ Adoption speed: Internet took 10+ years to reach mass adoption; AI reached 100M+ users in months

❌ Technology maturity: Early internet was clunky; current AI actually works remarkably well

❌ Infrastructure exists: Dot-com required building entire internet infrastructure; AI leverages existing cloud/mobile infrastructure

❌ Real productivity gains: Internet eventually delivered on promises (just took longer); AI already showing measurable ROI in many applications

What happened after the dot-com crash:

- Short-term: Brutal. 80% decline in NASDAQ, mass layoffs, thousands of companies bankrupt

- Medium-term (2003-2007): Recovery as real internet businesses emerged (Google, Amazon, eBay thrived)

- Long-term: The internet bulls were right—but 90% of the 2000-era companies died before seeing it

The key insight:

Technology revolutions often happen on the timeline predicted, but not with the companies initially hyped. The internet transformed everything, just not via Pets.com and Webvan.

AI will likely follow the same pattern: Transformative technology, correct direction, but most 2026-era AI companies won’t exist in 2030.

Forbes’ Gil Press sums it up:

“The collection and analysis of data was formalized in statistics centuries before computers. AI is nothing more than the latest stage in the evolution of the modern computer, gradually expanding automation. We’ve seen bubbles before. This is ‘a $2.52 trillion AI bubble’ now, just as there was an internet bubble. The question isn’t if AI transforms work—it’s when, how, and which companies survive.“

What You Should Do Right Now

For Individual Professionals

This week:

✅ Audit your job’s “AI replaceability score”: Are you doing tasks Claude Cowork already handles?

✅ Start using AI agents daily: Hands-on experience is the only way to understand their capabilities and limitations

✅ Document your strategic value: Build case studies showing where human judgment outperforms AI

This month:

✅ Develop AI orchestration skills: Learn to delegate to AI effectively

✅ Network in AI-resistant domains: Build relationships in areas where humans remain essential

✅ Financial stress test: Model your finances assuming 30% income reduction or job loss

This quarter:

✅ Consider career pivot: If your role is highly automatable, start transitioning now before labor market floods

✅ Build personal brand: Establish expertise and visibility so you’re not competing with anonymous candidates

For Investors

Conservative strategy:

- Reduce exposure to pure-play SaaS with weak moats

- Increase cash position to 20-30% of portfolio

- Diversify out of Magnificent 7 concentration

- Buy put options on software ETFs as insurance

- Wait for capitulation signals before deploying capital

Aggressive strategy:

- Short vulnerable SaaS (note: crowded trade, manage risk)

- Go long AI infrastructure (chips, data centers, energy)

- Bet on AI-native pivots (companies rebuilding around agents)

- Play volatility through options strategies

What NOT to do:

❌ Panic sell everything

❌ Double down on falling knives hoping for mean reversion

❌ Ignore the trend and assume “this too shall pass”

❌ Trust analyst price targets based on pre-AI business models

For Business Leaders

Immediate actions (Next 2 weeks):

- Emergency strategy session with C-suite on AI agent implications

- Contact your largest SaaS vendors and renegotiate terms

- Identify 3 workflows to pilot with AI agents

- Hire or designate an “AI strategy lead”

Short-term (Next 90 days):

- Run controlled experiments measuring AI agent productivity vs. existing tools

- Assess which roles will be augmented vs. replaced

- Communicate transparently with employees about AI adoption plans

- Build scenario models for 30%, 50%, and 70% reduction in SaaS spending

Medium-term (Rest of 2026):

- Pivot to AI-native workflows where pilots prove successful

- Reskill workforce for AI oversight and strategic roles

- Explore custom AI agent development now that costs have dropped 10-100x

- Prepare for margin expansion as productivity increases with fewer tools/seats

Five Predictions for the Rest of 2026

1. Software Stocks Find a Bottom… Eventually

Prediction: Software sector decline continues through Q1, bottoms in Q2, begins recovery in Q3.

Why: Current panic is partially justified but overdone. Companies will demonstrate which business models survive AI agents, and markets will stabilize around new valuation paradigms.

What to watch: Quarterly earnings in April-May will be critical. Revenue growth + margin resilience = survivors.

2. Mass SaaS Consolidation Begins

Prediction: 30%+ of pure-play SaaS companies acquired or go bankrupt by year-end.

Why: Weak-moat SaaS tools can’t justify standalone valuations when agents replicate their functionality. Larger platforms will acquire features/customers at fire-sale prices.

What to watch: M&A activity accelerates in Q2-Q3 as distressed valuations create opportunities.

3. “AI-Native” Becomes Table Stakes

Prediction: By Q4, every major software company claims to be “AI-native” with agent-first workflows.

Why: Market punishes companies perceived as vulnerable to disruption. Only way to stop the bleeding is demonstrate AI integration.

What to watch: Product launches, rebranding, acquisitions of AI startups. Some will be genuine pivots, most will be marketing spin.

4. The Magnificent 7 Fractures

Prediction: Market concentration decreases as differentiation emerges between infrastructure winners (Nvidia, Microsoft, Google) and AI application companies facing pressure.

Why: Not all tech is equal in an AI-first world. Companies selling AI tools will be valued differently than companies using AI to enhance existing moats.

What to watch: Relative performance of Nvidia/Microsoft vs. Meta/Tesla as proxies for infrastructure vs. application plays.

5. Employment Effects Become Visible

Prediction: White-collar job cuts accelerate in Q2-Q3, particularly in roles like:

- Junior analysts and researchers

- Customer support representatives

- Administrative assistants

- Junior lawyers and paralegals

- Entry-level marketing roles

Why: AI agents are already demonstrating 80%+ time savings on these tasks. Companies facing revenue pressure will cut headcount to maintain margins.

What to watch: Tech sector layoff announcements, unemployment data for knowledge workers, changes in job postings for entry-level roles.

The Bottom Line: This Is Real, But Not Simple

The software sector selloff isn’t pure panic, and it’s not pure rationality. It’s a market trying to price in a future where:

✅ AI agents can automate entire workflows, not just individual tasks

✅ Business models built on per-seat pricing are under threat

✅ Trillions in market value depend on AI delivering on its promises

✅ The line between “AI-augmented” and “AI-replaced” is unclear

What we know for certain:

- Claude Cowork and similar AI agents can already do remarkable things that required expensive software tools weeks ago

- Software companies will face pricing pressure and margin compression even if they aren’t completely replaced

- The $30 trillion at risk estimate isn’t fearmongering—it’s basic math on what happens if AI valuations correct like dot-com

- Some software companies will survive and thrive; most won’t

- Employees in automatable roles face real displacement risk within 12-18 months

What remains uncertain:

❓ Will AI agents prove reliable enough for mission-critical workflows?

❓ Can software companies pivot to AI-native models fast enough?

❓ Will regulatory/compliance requirements slow AI adoption?

❓ Is the $2.52 trillion AI spending sustainable or a bubble?

❓ How long until the next “Claude Cowork moment” triggers another wave of panic?

The strategic imperative:

Don’t panic. Don’t ignore. Adapt.

Run experiments. Gather data. Make decisions based on what AI can actually do in your specific context, not on hype or fear.

The companies and individuals who figure this out in the next 90 days will have an enormous advantage over those who wait for certainty that will never arrive.

The AI revolution isn’t coming. It arrived last week. The question is: What are you going to do about it?

How Kersai Can Help You Navigate the AI Disruption

At Kersai, we help organizations and individuals cut through AI hype and make strategic decisions based on real capabilities, not marketing promises.

For Businesses: AI Strategy & Implementation

- AI agent pilot programs: Test Claude Cowork, GPT-5.3-Codex, and alternatives on your workflows

- SaaS replacement roadmaps: Identify which tools can be replaced by agents and which can’t

- Workforce transition planning: Reskill teams for AI oversight and strategic roles

- ROI measurement: Track actual productivity gains vs. costs

- Vendor negotiation support: Leverage market conditions to renegotiate SaaS contracts

For Investors: Market Intelligence & Analysis

- Sector analysis: Which software companies have defensible moats vs. vulnerable to disruption

- Scenario modeling: Quantify downside risk under different AI adoption curves

- Opportunity identification: Find AI-native companies and infrastructure plays

- Portfolio stress testing: Assess exposure to AI-related concentration risk

For Professionals: Career Strategy & Skills

- AI replaceability assessment: Evaluate your role’s vulnerability to automation

- Skills development: Learn AI orchestration, prompt engineering, and agent management

- Career pivoting: Identify AI-resistant domains and plan transitions

- Personal brand building: Establish expertise that differentiates you from AI

Thought Leadership & Content

- Expert AI analysis: We translate complex AI developments into strategic insights

- Authority building: Position your brand as a trusted voice on AI and emerging technology

- SEO-optimized content: Drive organic traffic with comprehensive, data-driven articles

Facing AI disruption and need expert guidance? Contact us to discuss your specific situation, or subscribe to our newsletter for weekly insights on AI developments, market analysis, and practical strategies for thriving in an AI-first world.

Key Takeaways

✅ S&P 500 Software Index down 19% over 8 days—worst losing streak in 6 years—wiping out $285B in single session

✅ Anthropic’s Claude Cowork triggered “SaaSapocalypse” panic by demonstrating agents can replace entire software workflows

✅ Oliver Wyman warns financial institutions could lose $30 trillion if AI bubble bursts like dot-com crash

✅ Nvidia CEO Jensen Huang calls the panic “most illogical thing in the world,” argues AI will use software tools, not replace them

✅ Analysts split between “AI will eat software” bears and “enterprises won’t abandon infrastructure” bulls

✅ Hedge funds have shorted $24 billion in software stocks in 2026 alone—5x increase from previous years

✅ AI infrastructure investment ($6+ trillion through 2030) accounted for 92% of U.S. GDP growth in H1 2025

✅ Some software companies will survive (mission-critical, deep data, regulated industries); most pure-play SaaS tools face existential threat

✅ White-collar job cuts expected to accelerate in Q2-Q3 as companies adopt AI agents showing 80%+ time savings

✅ Historical parallel to dot-com bubble: Technology was transformative, direction correct, but 90% of hyped companies died

Frequently Asked Questions

Is Claude Cowork really as powerful as the hype suggests?

Yes and no. Claude Cowork can genuinely automate complex workflows that previously required multiple software tools and human coordination. Early testers report 80%+ time savings on tasks like contract review, RFP responses, and Tier 1 support. However, it’s not perfect—it makes mistakes, requires human oversight for high-stakes decisions, and struggles with ambiguous instructions. The capability is real; the question is how quickly it improves and becomes reliable enough for mission-critical use.

Should I sell my software stocks immediately?

That depends on which stocks you own and your investment timeline. Pure-play SaaS tools with weak moats (project management, basic CRM, simple analytics) face genuine existential risk. Mission-critical enterprise software with deep customer data, regulatory requirements, and network effects (SAP, Oracle, ServiceNow) have better survival odds. Consider reducing exposure to vulnerable names, but don’t panic-sell everything—markets often overreact in both directions.

Is my job safe from AI automation?

It depends on your role. Jobs most at risk: junior analysts, customer support, administrative assistants, entry-level legal/marketing roles—anything that’s primarily information processing with clear inputs/outputs. Jobs least at risk: complex problem-solving requiring context and judgment, creative work, human relationship management, strategic planning, roles requiring physical presence. The key question: Can Claude Cowork do 80% of your job right now? If yes, start developing AI-orchestration skills or pivot to less automatable work.

Will the entire software industry collapse?

No. Software isn’t going away; it’s transforming. The “per-seat SaaS model” where companies pay $500-$2,000 per user per year for each tool is under threat. But software companies that pivot to “AI-native” models—building tools optimized for AI agents rather than human interfaces, or providing the data/infrastructure AI agents need—can survive and thrive. Think of it as the shift from desktop software (Microsoft Office) to cloud SaaS (Google Workspace)—disruptive but not apocalyptic.

What’s the difference between this and previous AI hype cycles?

This time, the technology actually works reliably. Previous AI winters happened because capabilities didn’t match promises (1980s expert systems, 2010s IBM Watson). Claude Cowork, GPT-5.3-Codex, and similar agents are demonstrating genuine productivity gains in real workflows today, not just demos. The hype may be excessive, valuations may be inflated, but the underlying capability is real and improving rapidly.

Could this trigger another 2008-style financial crisis?

Possibly, if the debt-fueled collapse scenario plays out. Oliver Wyman warns that banks may have far more exposure to AI-related infrastructure risk than they realize, similar to how banks underestimated housing exposure before 2008. Key warning signs: hyperscale tech companies issued $100+ billion in bonds in past 6 months (5x previous years); $1+ trillion in AI-related private credit debt expected. If AI ROI doesn’t materialize and defaults begin, contagion could spread. But we’re not there yet.

What should businesses do right now?

Three things immediately: (1) Pilot AI agents on non-critical workflows to gather real data on capabilities vs. marketing claims. (2) Renegotiate SaaS contracts for shorter terms and better pricing, citing market conditions. (3) Develop an “AI strategy” function with clear ownership and budget. Don’t panic and rip out your entire software stack, but don’t ignore this either. Run controlled experiments and make decisions based on evidence from your specific context.

About the Author: This analysis was prepared by Kersai’s AI research team, combining market analysis, technical assessment, and strategic implications for businesses, investors, and professionals navigating AI disruption. We help organizations and individuals make data-driven decisions in rapidly evolving technology landscapes.